WINNIPEG, Manitoba, August 5, 2015 /CNW/ — Pollard Banknote Limited (TSX: PBL) (“Pollard”) today released its financial results for the three months year ended June 30, 2015, with continuing strong trends in revenue, EBITDA and cash flow.

“We are pleased with our second quarter results, particularly in reference to a strong comparable from the second quarter 2014,” commented Co-Chief Executive Officer John Pollard. “Our volumes remained high and our continuing process improvement initiatives have helped us maintain strong earnings and generate significant cash flow, allowing us to continue to fund our new press expansion from internal sources.”

Our revenue exceeded $50 million for the second quarter in a row and our EBITDA was in excess of $6.3 million, a level consistent with the last number of quarters. In addition, for the second quarter in a row, our operations generated significant positive cash flow allowing us to maintain our strong balance sheet.”

“We are very excited that our new Tresu press is completing the final commissioning process and will shortly be printing live tickets for our customers. This new press provides us with leading edge print capabilities that will allow us to continue to push the envelope on premium, eye-catching consumer friendly lottery products and we look forward to increasing our volumes in the months and years to come. Our new press will also provide a lower cost structure.”

“The lottery industry remains in a very robust growth mode, with our clients looking at new revenue opportunities on almost a daily basis,” stated Co-Chief Executive Officer Doug Pollard. “iLottery offerings and other internet related products and solutions remain top of mind for many lottery directors and we feel our offerings in these areas have been very well received.”

“Equally satisfying however is the ongoing strong, underlying growth in the traditional paper based instant tickets, even in jurisdictions where iLottery sales have grown. Our Michigan Lottery iLottery business continues to be the leader in North America and we look forward to leveraging this success into more opportunities with other jurisdictions in the coming months.”

John Pollard concluded, “We continue to be very optimistic about the opportunities presented to our organization in both our traditional product offerings as well as newer areas such as iLottery, loyalty clubs, digital apps and other expanding services focused on growing our customers’ businesses and improving the experience for the consumers.”

POLLARD BANKNOTE LIMITED

Pollard is one of the leading providers of products and services to lottery and charitable gaming industries throughout the world. Management believes Pollard is the largest provider of instant tickets based in Canada and the second largest producer of instant tickets in the world.

The selected financial and operating information has been derived from, and should be read in conjunction with, the condensed consolidated unaudited interim financial statements of Pollard as at and for the three and six months ended June 30, 2015. These financial statements have been prepared in accordance with the International Financial Accounting Standards (“IFRS” or “GAAP”).

Results of Operations – Three months ended June 30, 2015

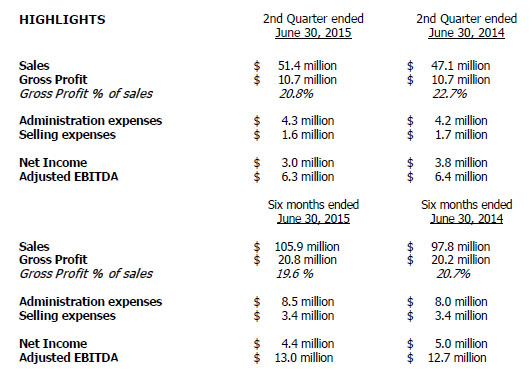

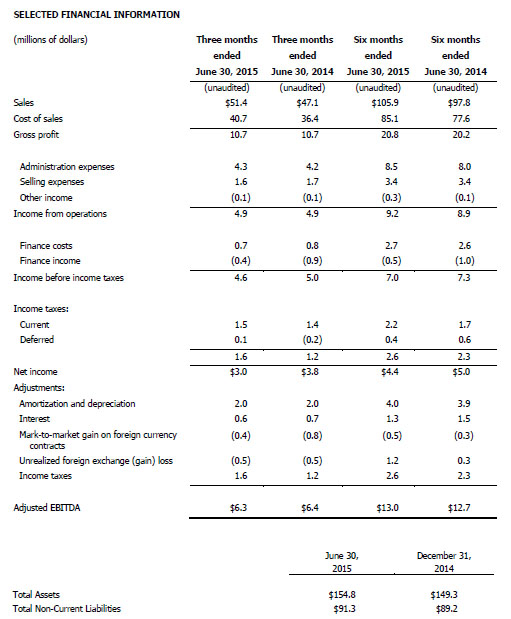

During the three months ended June 30, 2015, Pollard achieved sales of $51.4 million, compared to $47.1 million in the three months ended June 30, 2014. Factors impacting the $4.3 million sales increase were:

Cost of sales was $40.7 million in the second quarter of 2015 compared to $36.4 million in the second quarter of 2014. Cost of sales were higher in the quarter relative to 2014 as a result of higher instant ticket and ancillary sales volumes and higher exchange rates on U.S. dollar transactions.

Gross profit was $10.7 million (20.8% of sales) in the second quarter of 2015 compared to $10.7 million (22.7% of sales) in the second quarter of 2014. This decrease in gross profit percentage was primarily the result of the decrease in the average selling price for instant tickets and a small decrease in production volumes from the record level reached in the second quarter of 2014. These decreases were partially offset by the impact of the weakening of the Canadian dollar.

Administration expenses were $4.3 million in the second quarter of 2015 which was similar to $4.2 million in the second quarter of 2014.

Selling expenses were $1.6 million in the second quarter of 2015 which was similar to $1.7 million in the second quarter of 2014.

Interest expense was $0.6 million in the second quarter of 2015 which was similar to $0.7 million in the second quarter of 2014.

The net foreign exchange gain was nil in the second quarter of 2015 compared to a net gain of $0.1 million in the second quarter of 2014. Within the 2015 net foreign exchange gain was an unrealized foreign exchange gain of $0.5 million, predominately a result of unrealized gain on U.S. dollar denominated debt (caused by the strengthening of the value of the Canadian dollar versus the U.S. dollar) in addition to an unrealized gain on other U.S. dollar denominated accounts payable. Offsetting the unrealized gain was a realized foreign exchange loss of $0.5 million relating to the decreased value on the collections of U.S. dollar denominated receivables and a realized loss on the conversion of U.S. dollars and Euros into Canadian dollars.

Within the 2014 net foreign exchange gain was an unrealized foreign exchange gain of $0.5 million, relating to a $0.7 million unrealized foreign exchange gain on U.S. dollar denominated debt and payables, partially offset by a $0.2 million unrealized foreign exchange loss on U.S. dollar denominated cash and receivables. Partially offsetting the unrealized gain was a realized foreign exchange loss of $0.4 million relating to the decreased value of the collections of U.S. dollar denominated receivables of $0.3 million and a $0.2 million realized loss on the conversion of U.S. dollars and Euros into Canadian dollars. These realized losses were partially offset by a $0.1 million realized gain relating to payments made on U.S. dollar and Euro denominated payables.

Adjusted EBITDA was $6.3 million in the second quarter of 2015 compared to $6.4 million in the second quarter of 2014. The primary reason for the decrease in Adjusted EBITDA of $0.1 million was the increased realized foreign exchange loss of $0.1 million.

Income tax expense was $1.6 million in the second quarter of 2015, an effective rate of 35.7%, which was higher than our expected effective rate of 26.7% due primarily to differences relating to the foreign exchange impact of Canadian dollar denominated debt in its U.S. subsidiaries. Pollard has capitalized its U.S. operations using intercompany Canadian dollar debt. The overall weakening of the Canadian dollar versus the U.S. dollar results in a future gain on debt repayment for U.S. tax purposes in the subsidiary, creating a deferred tax expense with no related income (as the loss is eliminated on consolidation).

Income tax expense was $1.2 million in the second quarter of 2014, an effective rate of 23.4%, similar to our expected tax rate of 26.7%.

Amortization and depreciation, including amortization of deferred financing costs and intangible assets and depreciation of property and equipment, totaled $2.0 million during the second quarter of 2015 which was similar to $2.0 million during the second quarter of 2014.

Net income decreased to $3.0 million in the second quarter of 2015 from $3.8 million in the second quarter of 2014. The primary reasons for the decrease of $0.8 million in net income were the reduction in the gain on the non-cash mark-to-market adjustment on foreign currency contracts of $0.4 million and increased income tax expense of $0.4 million.

Net income per share (basic and diluted) decreased to $0.13 per share in the second quarter of 2015 from $0.16 per share in the second quarter of 2014.

Results of Operations – Six months ended June 30, 2015

During the six months ended June 30, 2015, Pollard achieved sales of $105.9 million, compared to $97.8 million in the six months ended June 30, 2014. Factors impacting the $8.1 million sales increase were:

Cost of sales was $85.1 million in the six months ended June 30, 2015, compared to $77.6 million in the six months ended June 30, 2014. Cost of sales was higher in the first half of 2015 relative to 2014 as a result of higher instant ticket sales volumes and higher exchange rates on U.S. dollar transactions.

Gross profit increased to $20.8 million (19.6% of sales) in the six months ended June 30, 2015, from $20.2 million (20.7% of sales) in the six months ended June 30, 2014. This increase was due mainly to the increase in instant ticket volumes as well as a result of the weakening of the Canadian dollar relative to the U.S. dollar. The decrease in gross profit percentage was primarily the result of the decrease in the average selling price for instant tickets and lower sales of ancillary instant ticket products, partially offset by the impact of the weakening of the Canadian dollar.

Administration expenses increased to $8.5 million in the first six months of 2015 from $8.0 million in the first six months of 2014 due primarily to increased compensation costs.

Selling expenses were $3.4 million in the first six months of 2015 which was similar to $3.4 million in the first six months of 2014.

Interest expense decreased to $1.3 million in the first six months of 2015 from $1.5 million in the first six months of 2014 as a result of lower interest rates.

The net foreign exchange loss was $1.2 million in the first six months of 2015 compared to a net loss of $0.3 million in the first half of 2014. The 2015 foreign exchange loss resulted from unrealized foreign exchange losses of $1.2 million, comprised predominately of an unrealized loss on U.S. dollar denominated debt (caused by the weakening of the value of the Canadian dollar versus the U.S. dollar) in addition to an unrealized loss on other U.S. dollar denominated accounts payable.

The 2014 foreign exchange loss resulted from unrealized foreign exchange losses of $0.3 million, comprised of $0.4 million unrealized foreign exchange loss on U.S. dollar denominated cash and accounts receivables, partially offset by $0.1 million unrealized gain on U.S. dollar denominated accounts payable.

Adjusted EBITDA was $13.0 million in the first six months of 2015 compared to $12.7 million in the first six months of 2014. The primary reason for the increase in Adjusted EBITDA of $0.3 million was the increased gross profit and other income, partially offset by increased administration expenses.

Income tax expense was $2.6 million in the first six months of 2015, an effective rate of 37.7%, which was higher than our expected effective rate of 26.7% due primarily to differences relating to the foreign exchange impact of Canadian dollar denominated debt in its U.S. subsidiaries. Pollard has capitalized its U.S. operations using intercompany Canadian dollar debt. The weakening of the Canadian dollar versus the U.S. dollar results in a future gain on debt repayment for U.S. tax purposes in the subsidiary, creating a deferred tax expense with no related income (as the gain is eliminated on consolidation). This increased the effective tax rate by about 16 percentage points. Other differences relating to permanent differences on the foreign exchange translation of property, plant and equipment, and other net liabilities decreased the effective tax rate by approximately 4 percentage points on a net basis.

Income tax expense was $2.3 million in the first six months of 2014, an effective rate of 31.6%, similar to our expected tax rate of 26.7%.

Amortization and depreciation, including amortization of deferred financing costs and intangible assets and depreciation of property and equipment, totaled $4.0 million during the first six months of 2015 which was similar to $3.9 million during the first six months of 2014.

Net income was $4.4 million in the first six months of 2015 compared to $5.0 million in the first six months of 2014. The primary reasons for the decrease of $0.6 million was higher administration expenses of $0.5 million, increase in net foreign exchange loss of $0.9 million and higher income tax expense of $0.3 million. These decreases were partially offset by an increase in gross profit of $0.6 million, the decrease in interest expense of $0.2 million and the increased gain on the non-cash mark-to-market adjustment on foreign currency contracts of $0.2 million.

Net income per share (basic and diluted) decreased to $0.18 per share in the six months ending June 30, 2015, as compared to $0.21 per share in the six months ending June 30, 2014.

Use of Non-GAAP Financial Measures

Reference to “Adjusted EBITDA” is to earnings before interest, income taxes, amortization and depreciation, unrealized foreign exchange gains and losses, mark-to-market gains and losses on foreign currency contracts, and certain non-recurring items including startup costs. Adjusted EBITDA is an important metric used by many investors to compare issuers on the basis of the ability to generate cash from operations and management believes that, in addition to net income, Adjusted EBITDA is a useful supplementary measure. <

Adjusted EBITDA is a measure not recognized under GAAP and does not have a standardized meaning prescribed by GAAP. Therefore, this measure may not be comparable to similar measures presented by other entities. Investors are cautioned that Adjusted EBITDA should not be construed as an alternative to net income determined in accordance with GAAP as an indicator of Pollard’s performance or to cash flows from operating, investing and financing activities as measures of liquidity and cash flows.

Outlook

As noted frequently in our previous outlooks the lottery industry continues to show strong growth with many individual lotteries establishing record sales with the completion of their fiscal years, generally June 30. One of the key drivers of this growth has been the strong sales of instant tickets and we believe this trend will remain. Consumer demand is strong for instant tickets and lotteries, in conjunction with their partners like Pollard, will continue to develop unique products to meet this growing demand.

Our expected volumes over the rest of 2015 will be consistent with the levels we have achieved over the past number of quarters, which were among the highest production levels ever experienced in our business.

Our new Tresu press is completing its final testing and will commence printing live product shortly. Over the next few quarters we will be transferring our existing production volumes from the current press in Ypsilanti to this new press, as well as developing additional volumes through attaining new work. The nature of the long sales cycle (multiyear contracts, formal RFP processes) in our industry results in a slow ramp up of additional volumes, so we are anticipating the full impact of our new capacity will not be felt for some period of time. In addition, the new press will provide for a lower cost of production.

Our expected levels of CAPEX should be reduced for the remainder of 2015 relative to the levels incurred over the last few quarters. There remains a number of additional phases to still complete, primarily the transfer of the existing press from Ypsilanti to Winnipeg. This is expected to occur over the final quarter of 2015 and the first quarter of 2016.

Our Michigan iLottery joint venture operation is maintaining its strong levels of results achieved since the formal launch in the fall of 2014. We are anticipating other opportunities to attain further iLottery related work moving forward as the lottery industry, particularly in the United States, look more and more for areas to grow their business. We believe we have a very positive track record with our current iLottery operations which should position us well for future business opportunities.

The Canadian dollar has remained weak relative to the U.S. dollar during 2015 which generates higher levels of cash flow due to our net exposure to U.S. dollar inflows. Continued weakness will have a positive impact on our cash flows, both in terms of greater amounts of Canadian dollars on conversion and allowing us to bid competitively for new work. We currently have no financial hedges in place offsetting this risk, with our last foreign exchange currency forward contract expiring in the second quarter. We have no plans currently to enter into any further foreign currency forward contracts. Recently the Canadian dollar has also weakened versus the Euro. We have a number of clients who pay us in Euros and the weakening dollar against this currency has impacted our cash flows positively.

We anticipate our internal operating cash flow over the next 12 months to generate sufficient funds to satisfy all of our requirements including the remaining capital expenditures relating to the completion of the remaining phases of the press line expansion. Our current credit facility was formally renewed at the end of the second quarter 2015, which provides flexibility and capacity to support our various strategic initiatives. All excess cash flow will be used to reduce our senior bank debt.

“We are pleased with our second quarter results, particularly in reference to a strong comparable from the second quarter 2014,” commented Co-Chief Executive Officer John Pollard. “Our volumes remained high and our continuing process improvement initiatives have helped us maintain strong earnings and generate significant cash flow, allowing us to continue to fund our new press expansion from internal sources.”

Our revenue exceeded $50 million for the second quarter in a row and our EBITDA was in excess of $6.3 million, a level consistent with the last number of quarters. In addition, for the second quarter in a row, our operations generated significant positive cash flow allowing us to maintain our strong balance sheet.”

“We are very excited that our new Tresu press is completing the final commissioning process and will shortly be printing live tickets for our customers. This new press provides us with leading edge print capabilities that will allow us to continue to push the envelope on premium, eye-catching consumer friendly lottery products and we look forward to increasing our volumes in the months and years to come. Our new press will also provide a lower cost structure.”

“The lottery industry remains in a very robust growth mode, with our clients looking at new revenue opportunities on almost a daily basis,” stated Co-Chief Executive Officer Doug Pollard. “iLottery offerings and other internet related products and solutions remain top of mind for many lottery directors and we feel our offerings in these areas have been very well received.”

“Equally satisfying however is the ongoing strong, underlying growth in the traditional paper based instant tickets, even in jurisdictions where iLottery sales have grown. Our Michigan Lottery iLottery business continues to be the leader in North America and we look forward to leveraging this success into more opportunities with other jurisdictions in the coming months.”

John Pollard concluded, “We continue to be very optimistic about the opportunities presented to our organization in both our traditional product offerings as well as newer areas such as iLottery, loyalty clubs, digital apps and other expanding services focused on growing our customers’ businesses and improving the experience for the consumers.”

POLLARD BANKNOTE LIMITED

Pollard is one of the leading providers of products and services to lottery and charitable gaming industries throughout the world. Management believes Pollard is the largest provider of instant tickets based in Canada and the second largest producer of instant tickets in the world.

The selected financial and operating information has been derived from, and should be read in conjunction with, the condensed consolidated unaudited interim financial statements of Pollard as at and for the three and six months ended June 30, 2015. These financial statements have been prepared in accordance with the International Financial Accounting Standards (“IFRS” or “GAAP”).

Results of Operations – Three months ended June 30, 2015

During the three months ended June 30, 2015, Pollard achieved sales of $51.4 million, compared to $47.1 million in the three months ended June 30, 2014. Factors impacting the $4.3 million sales increase were:

- Instant ticket sales volumes, including sales of ancillary instant ticket products and services, increased when compared to the second quarter of 2014, increasing sales by $1.7 million. Instant ticket average selling price decreased in the second quarter of 2015 compared to the prior year which reduced sales by $1.0 million. Charitable gaming volume decreased slightly during the quarter reducing sales by $0.4 million when compared to 2014, while a decrease in the charitable gaming average selling price further reduced sales by $0.1 million when compared to the second quarter of 2014. An increase in machine volumes increased sales by $0.1 million in the second quarter of 2015 as compared to the prior year.

- During the three months ended June 30, 2015, Pollard generated approximately 68.5% (2014 – 60.5%) of its revenue in U.S. dollars including a portion of international sales which are priced in U.S. dollars. During the second quarter of 2015 the actual U.S. dollar value was converted to Canadian dollars at $1.238, compared to a rate of $1.080 during the second quarter of 2014. This 14.7% increase in the U.S. dollar value resulted in an approximate increase of $4.5 million in revenue relative to the second quarter of 2014. Also during the quarter, the value of the Euro weakened against the Canadian dollar resulting in an approximate decrease of $0.5 million in revenue relative to the second quarter of 2014.

Cost of sales was $40.7 million in the second quarter of 2015 compared to $36.4 million in the second quarter of 2014. Cost of sales were higher in the quarter relative to 2014 as a result of higher instant ticket and ancillary sales volumes and higher exchange rates on U.S. dollar transactions.

Gross profit was $10.7 million (20.8% of sales) in the second quarter of 2015 compared to $10.7 million (22.7% of sales) in the second quarter of 2014. This decrease in gross profit percentage was primarily the result of the decrease in the average selling price for instant tickets and a small decrease in production volumes from the record level reached in the second quarter of 2014. These decreases were partially offset by the impact of the weakening of the Canadian dollar.

Administration expenses were $4.3 million in the second quarter of 2015 which was similar to $4.2 million in the second quarter of 2014.

Selling expenses were $1.6 million in the second quarter of 2015 which was similar to $1.7 million in the second quarter of 2014.

Interest expense was $0.6 million in the second quarter of 2015 which was similar to $0.7 million in the second quarter of 2014.

The net foreign exchange gain was nil in the second quarter of 2015 compared to a net gain of $0.1 million in the second quarter of 2014. Within the 2015 net foreign exchange gain was an unrealized foreign exchange gain of $0.5 million, predominately a result of unrealized gain on U.S. dollar denominated debt (caused by the strengthening of the value of the Canadian dollar versus the U.S. dollar) in addition to an unrealized gain on other U.S. dollar denominated accounts payable. Offsetting the unrealized gain was a realized foreign exchange loss of $0.5 million relating to the decreased value on the collections of U.S. dollar denominated receivables and a realized loss on the conversion of U.S. dollars and Euros into Canadian dollars.

Within the 2014 net foreign exchange gain was an unrealized foreign exchange gain of $0.5 million, relating to a $0.7 million unrealized foreign exchange gain on U.S. dollar denominated debt and payables, partially offset by a $0.2 million unrealized foreign exchange loss on U.S. dollar denominated cash and receivables. Partially offsetting the unrealized gain was a realized foreign exchange loss of $0.4 million relating to the decreased value of the collections of U.S. dollar denominated receivables of $0.3 million and a $0.2 million realized loss on the conversion of U.S. dollars and Euros into Canadian dollars. These realized losses were partially offset by a $0.1 million realized gain relating to payments made on U.S. dollar and Euro denominated payables.

Adjusted EBITDA was $6.3 million in the second quarter of 2015 compared to $6.4 million in the second quarter of 2014. The primary reason for the decrease in Adjusted EBITDA of $0.1 million was the increased realized foreign exchange loss of $0.1 million.

Income tax expense was $1.6 million in the second quarter of 2015, an effective rate of 35.7%, which was higher than our expected effective rate of 26.7% due primarily to differences relating to the foreign exchange impact of Canadian dollar denominated debt in its U.S. subsidiaries. Pollard has capitalized its U.S. operations using intercompany Canadian dollar debt. The overall weakening of the Canadian dollar versus the U.S. dollar results in a future gain on debt repayment for U.S. tax purposes in the subsidiary, creating a deferred tax expense with no related income (as the loss is eliminated on consolidation).

Income tax expense was $1.2 million in the second quarter of 2014, an effective rate of 23.4%, similar to our expected tax rate of 26.7%.

Amortization and depreciation, including amortization of deferred financing costs and intangible assets and depreciation of property and equipment, totaled $2.0 million during the second quarter of 2015 which was similar to $2.0 million during the second quarter of 2014.

Net income decreased to $3.0 million in the second quarter of 2015 from $3.8 million in the second quarter of 2014. The primary reasons for the decrease of $0.8 million in net income were the reduction in the gain on the non-cash mark-to-market adjustment on foreign currency contracts of $0.4 million and increased income tax expense of $0.4 million.

Net income per share (basic and diluted) decreased to $0.13 per share in the second quarter of 2015 from $0.16 per share in the second quarter of 2014.

Results of Operations – Six months ended June 30, 2015

During the six months ended June 30, 2015, Pollard achieved sales of $105.9 million, compared to $97.8 million in the six months ended June 30, 2014. Factors impacting the $8.1 million sales increase were:

- Instant ticket sales volumes increased sales by $5.4 million when compared to 2014 while lower sales of our ancillary instant ticket products and services reduced sales by $2.4 million from the first half of 2014. Lower instant ticket average selling price decreased sales by $1.9 million in the first six months of 2015 compared to the first six months of 2014. Charitable gaming products volumes were lower than the first six months of 2014 which decreased sales by $0.8 million. An increase in machine volumes increased sales by $0.3 million in the six months ending June 30, 2015 as compared to the prior year.

- During the six months ended June 30, 2015, Pollard generated approximately 68.2% (2014 – 65.5%) of its revenue in U.S. dollars including a portion of international sales which are priced in U.S. dollars. During the first six months of 2015 the actual U.S. dollar value was converted to Canadian dollars at $1.226, compared to a rate of $1.087 during the first six months of 2014. This 12.8% increase in the U.S. dollar value resulted in an approximate increase of $8.2 million in revenue relative to the six months ended June 30, 2014. Also during the first half of 2015, the value of the Euro weakened against the Canadian dollar resulting in an approximate decrease of $0.7 million in revenue relative to the first half of 2014.

Cost of sales was $85.1 million in the six months ended June 30, 2015, compared to $77.6 million in the six months ended June 30, 2014. Cost of sales was higher in the first half of 2015 relative to 2014 as a result of higher instant ticket sales volumes and higher exchange rates on U.S. dollar transactions.

Gross profit increased to $20.8 million (19.6% of sales) in the six months ended June 30, 2015, from $20.2 million (20.7% of sales) in the six months ended June 30, 2014. This increase was due mainly to the increase in instant ticket volumes as well as a result of the weakening of the Canadian dollar relative to the U.S. dollar. The decrease in gross profit percentage was primarily the result of the decrease in the average selling price for instant tickets and lower sales of ancillary instant ticket products, partially offset by the impact of the weakening of the Canadian dollar.

Administration expenses increased to $8.5 million in the first six months of 2015 from $8.0 million in the first six months of 2014 due primarily to increased compensation costs.

Selling expenses were $3.4 million in the first six months of 2015 which was similar to $3.4 million in the first six months of 2014.

Interest expense decreased to $1.3 million in the first six months of 2015 from $1.5 million in the first six months of 2014 as a result of lower interest rates.

The net foreign exchange loss was $1.2 million in the first six months of 2015 compared to a net loss of $0.3 million in the first half of 2014. The 2015 foreign exchange loss resulted from unrealized foreign exchange losses of $1.2 million, comprised predominately of an unrealized loss on U.S. dollar denominated debt (caused by the weakening of the value of the Canadian dollar versus the U.S. dollar) in addition to an unrealized loss on other U.S. dollar denominated accounts payable.

The 2014 foreign exchange loss resulted from unrealized foreign exchange losses of $0.3 million, comprised of $0.4 million unrealized foreign exchange loss on U.S. dollar denominated cash and accounts receivables, partially offset by $0.1 million unrealized gain on U.S. dollar denominated accounts payable.

Adjusted EBITDA was $13.0 million in the first six months of 2015 compared to $12.7 million in the first six months of 2014. The primary reason for the increase in Adjusted EBITDA of $0.3 million was the increased gross profit and other income, partially offset by increased administration expenses.

Income tax expense was $2.6 million in the first six months of 2015, an effective rate of 37.7%, which was higher than our expected effective rate of 26.7% due primarily to differences relating to the foreign exchange impact of Canadian dollar denominated debt in its U.S. subsidiaries. Pollard has capitalized its U.S. operations using intercompany Canadian dollar debt. The weakening of the Canadian dollar versus the U.S. dollar results in a future gain on debt repayment for U.S. tax purposes in the subsidiary, creating a deferred tax expense with no related income (as the gain is eliminated on consolidation). This increased the effective tax rate by about 16 percentage points. Other differences relating to permanent differences on the foreign exchange translation of property, plant and equipment, and other net liabilities decreased the effective tax rate by approximately 4 percentage points on a net basis.

Income tax expense was $2.3 million in the first six months of 2014, an effective rate of 31.6%, similar to our expected tax rate of 26.7%.

Amortization and depreciation, including amortization of deferred financing costs and intangible assets and depreciation of property and equipment, totaled $4.0 million during the first six months of 2015 which was similar to $3.9 million during the first six months of 2014.

Net income was $4.4 million in the first six months of 2015 compared to $5.0 million in the first six months of 2014. The primary reasons for the decrease of $0.6 million was higher administration expenses of $0.5 million, increase in net foreign exchange loss of $0.9 million and higher income tax expense of $0.3 million. These decreases were partially offset by an increase in gross profit of $0.6 million, the decrease in interest expense of $0.2 million and the increased gain on the non-cash mark-to-market adjustment on foreign currency contracts of $0.2 million.

Net income per share (basic and diluted) decreased to $0.18 per share in the six months ending June 30, 2015, as compared to $0.21 per share in the six months ending June 30, 2014.

Use of Non-GAAP Financial Measures

Reference to “Adjusted EBITDA” is to earnings before interest, income taxes, amortization and depreciation, unrealized foreign exchange gains and losses, mark-to-market gains and losses on foreign currency contracts, and certain non-recurring items including startup costs. Adjusted EBITDA is an important metric used by many investors to compare issuers on the basis of the ability to generate cash from operations and management believes that, in addition to net income, Adjusted EBITDA is a useful supplementary measure. <

Adjusted EBITDA is a measure not recognized under GAAP and does not have a standardized meaning prescribed by GAAP. Therefore, this measure may not be comparable to similar measures presented by other entities. Investors are cautioned that Adjusted EBITDA should not be construed as an alternative to net income determined in accordance with GAAP as an indicator of Pollard’s performance or to cash flows from operating, investing and financing activities as measures of liquidity and cash flows.

Outlook

As noted frequently in our previous outlooks the lottery industry continues to show strong growth with many individual lotteries establishing record sales with the completion of their fiscal years, generally June 30. One of the key drivers of this growth has been the strong sales of instant tickets and we believe this trend will remain. Consumer demand is strong for instant tickets and lotteries, in conjunction with their partners like Pollard, will continue to develop unique products to meet this growing demand.

Our expected volumes over the rest of 2015 will be consistent with the levels we have achieved over the past number of quarters, which were among the highest production levels ever experienced in our business.

Our new Tresu press is completing its final testing and will commence printing live product shortly. Over the next few quarters we will be transferring our existing production volumes from the current press in Ypsilanti to this new press, as well as developing additional volumes through attaining new work. The nature of the long sales cycle (multiyear contracts, formal RFP processes) in our industry results in a slow ramp up of additional volumes, so we are anticipating the full impact of our new capacity will not be felt for some period of time. In addition, the new press will provide for a lower cost of production.

Our expected levels of CAPEX should be reduced for the remainder of 2015 relative to the levels incurred over the last few quarters. There remains a number of additional phases to still complete, primarily the transfer of the existing press from Ypsilanti to Winnipeg. This is expected to occur over the final quarter of 2015 and the first quarter of 2016.

Our Michigan iLottery joint venture operation is maintaining its strong levels of results achieved since the formal launch in the fall of 2014. We are anticipating other opportunities to attain further iLottery related work moving forward as the lottery industry, particularly in the United States, look more and more for areas to grow their business. We believe we have a very positive track record with our current iLottery operations which should position us well for future business opportunities.

The Canadian dollar has remained weak relative to the U.S. dollar during 2015 which generates higher levels of cash flow due to our net exposure to U.S. dollar inflows. Continued weakness will have a positive impact on our cash flows, both in terms of greater amounts of Canadian dollars on conversion and allowing us to bid competitively for new work. We currently have no financial hedges in place offsetting this risk, with our last foreign exchange currency forward contract expiring in the second quarter. We have no plans currently to enter into any further foreign currency forward contracts. Recently the Canadian dollar has also weakened versus the Euro. We have a number of clients who pay us in Euros and the weakening dollar against this currency has impacted our cash flows positively.

We anticipate our internal operating cash flow over the next 12 months to generate sufficient funds to satisfy all of our requirements including the remaining capital expenditures relating to the completion of the remaining phases of the press line expansion. Our current credit facility was formally renewed at the end of the second quarter 2015, which provides flexibility and capacity to support our various strategic initiatives. All excess cash flow will be used to reduce our senior bank debt.